What’s Driving Firms Forward This Year?

The accounting profession looks a lot different than it did even last year, and the pace of change isn’t slowing down. Between the rapid adoption of AI, growing client demand for strategic guidance, and an increasingly dangerous cybersecurity landscape, firms are being pushed to rethink not just the services they offer, but how they operate from the ground up.

The good news? Firms that are willing to evolve are finding real opportunities to grow revenue, deepen client relationships, and build a more resilient business. The not-so-good news? Standing still isn’t really an option anymore. The gap between firms that embrace these shifts and those that resist them is widening fast.

This article will cover the four trends shaping the accounting profession in 2026 and what they mean for your firm.

Table of Contents

- The Rise of Advisory Services

- AI for Productivity

- Changing Tech Stacks

- New Security Threats

- The Bottom Line

1. The Rise of Advisory Services

Clients don’t just want someone to crunch their numbers anymore. They want a trusted partner who can help them plan for what’s next. From financial planning and cash flow forecasting to tax strategy and business consulting, the expectations clients bring to their accounting firm have evolved significantly. And firms that are stepping up to meet those expectations? They’re being rewarded with stronger client retention and higher revenue per engagement.

It’s a genuine win-win: Clients get the strategic guidance they need to grow and make smarter decisions, while accountants expand their service portfolio, deepen their client relationships, and boost their bottom line.

This shift is also changing what it means to be a great accountant. Today’s advisory-ready professionals need a broader skill set—one that goes beyond technical know-how to include data interpretation, industry-specific insight, and the communication skills to translate complex financial information into clear, actionable advice.

Expanding into advisory also means handling more sensitive client data across more touchpoints. This demands stronger security protections and streamlined technology that can support increased workflows without adding complexity. Firms are investing in advisory-focused training, tightening their security posture, and restructuring their service tiers to lead with strategic guidance rather than tacking it on as an afterthought.

2. AI for Productivity

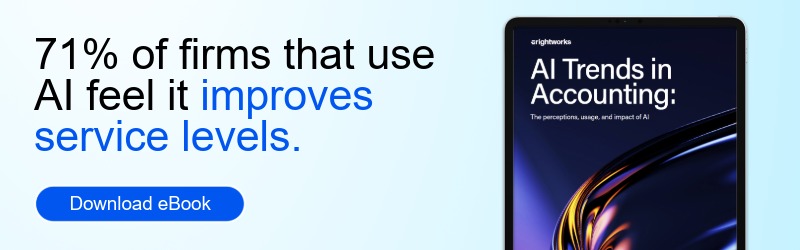

Artificial intelligence is no longer a futuristic concept in accounting. It’s an everyday productivity tool, and the impact is already measurable. Firms actively using AI reported 37% higher revenue per employee compared to those not using it. And when asked about the biggest benefits, the top responses were time savings (66%) and task automation (64%). About half of the respondents said AI saves them two or more hours per week, time that can be redirected toward the kind of advisory and client-facing work that drives growth.

However, the integration of AI into accounting workflows also demands a shift in professional competence. Accountants must develop a working understanding of how AI models generate outputs, where they’re prone to error, and how to validate machine-generated results against professional standards. Firms that treat AI as a “set it and forget it” solution risk compliance failures and reputational damage. The most successful adopters are those that pair AI automation with robust human oversight, using the technology to enhance, not replace, professional judgment.

3. Changing Tech Stacks

The accounting technology landscape is undergoing a fundamental transformation as firms move away from legacy desktop software toward integrated cloud platforms. Modern tech stacks increasingly feature connected ecosystems where accounting software, payroll, expense management, client portals, and reporting tools share data seamlessly in real time. This shift is enabling firms to eliminate redundant data entry, improve collaboration with clients, and safely access financial information from anywhere, which is an expectation that has become non-negotiable in the post-pandemic workplace.

Choosing and managing these evolving tech stacks has become a strategic decision in itself. Firms must evaluate:

- The features of individual tools

- How well they integrate with one another

- How they handle data migration

- Whether they can scale with the firm’s growth

Many firms are appointing dedicated technology leads or partnering with IT consultants to manage this transition. Those that fail to modernize risk falling behind competitors who can deliver faster turnaround times, more transparent reporting, and a smoother client experience through their technology infrastructure.

Related Article → How to Optimize Your Firm’s Tech Stack and Eliminate App Sprawl

4. New Security Threats

As accounting firms digitize their operations and store increasing volumes of sensitive financial data in the cloud, they have become prime targets for cybercriminals. In fact, 88% of organizations experienced at least one trust-undermining incident in the past year.

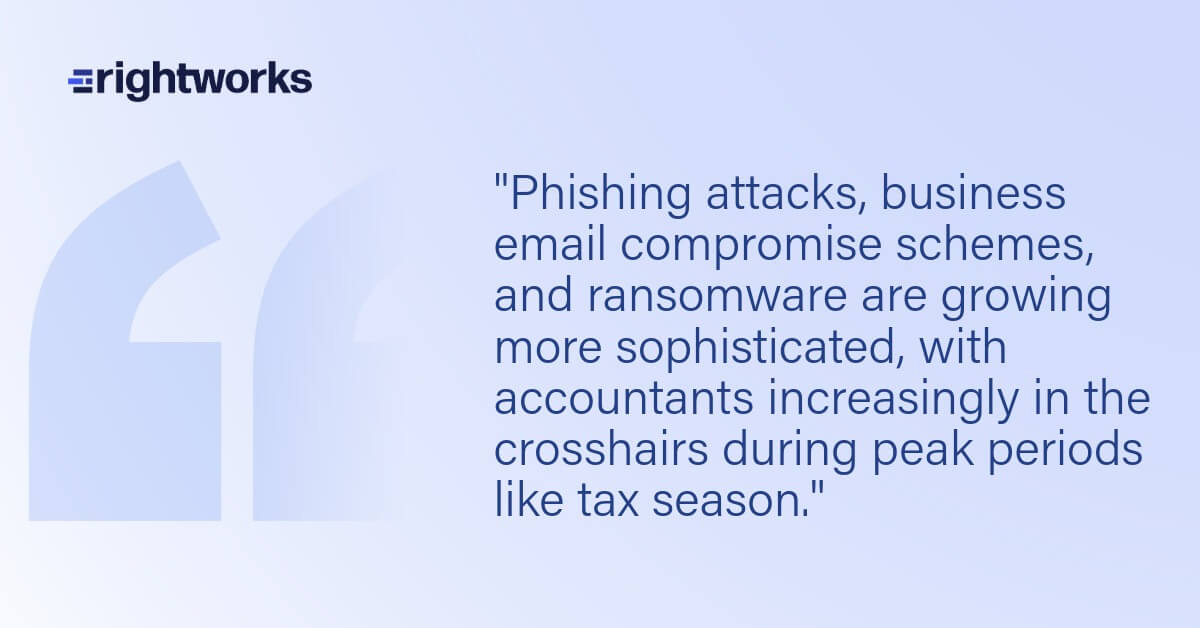

Phishing attacks, business email compromise schemes, and ransomware are growing more sophisticated, with accountants increasingly in the crosshairs during peak periods like tax season. The stakes are exceptionally high. A single breach can expose client tax identification numbers, bank account details, and confidential business financials, leading to regulatory penalties, lawsuits, and devastating reputational harm.

In response, firms must treat cybersecurity as a core business function rather than an IT afterthought.

Key measures include:

- Multifactor authentication and end-to-end encryption to protect client data at every access point.

- Zero-trust network architecture, which assumes no user or device is automatically trusted and requires verification at every step, limiting exposure if a breach does occur.

- Regular staff training on threat recognition, especially during high-risk periods like tax season.

- Compliance with evolving data protection regulations that hold accounting firms to increasingly strict standards of care.

Firms that proactively invest in security infrastructure and cultivate a culture of cyber awareness will not only protect themselves from financial loss but will also build a competitive advantage, as clients increasingly factor data security into their decisions when choosing an accounting partner.

The Bottom Line

The common thread across all four trends? Governance, access management, and centralized control. Whether you’re rolling out AI, migrating platforms, or defending against cyberthreats, success comes down to visibility into your systems, control over access, and the ability to enforce policies consistently.

Firms that embrace these trends with proper planning and governance will thrive. Those that resist—or adopt new tools without the right controls—will find it harder to compete for both talent and clients.